Guest editorial

By Dr. Albert D. Bates, Principal, Distribution Performance Project

This article was published in the October 2019 edition of NTEA News.

One of the oldest and best adages in business is that nothing happens until somebody sells something. The way those sales are generated, however, is often overlooked. In fact, different ways of producing the same sales volume can lead to substantially varying levels of profit.

This article examines the financial impact of two different methods for increasing sales — selling more physical merchandise and raising prices on merchandise already being sold.

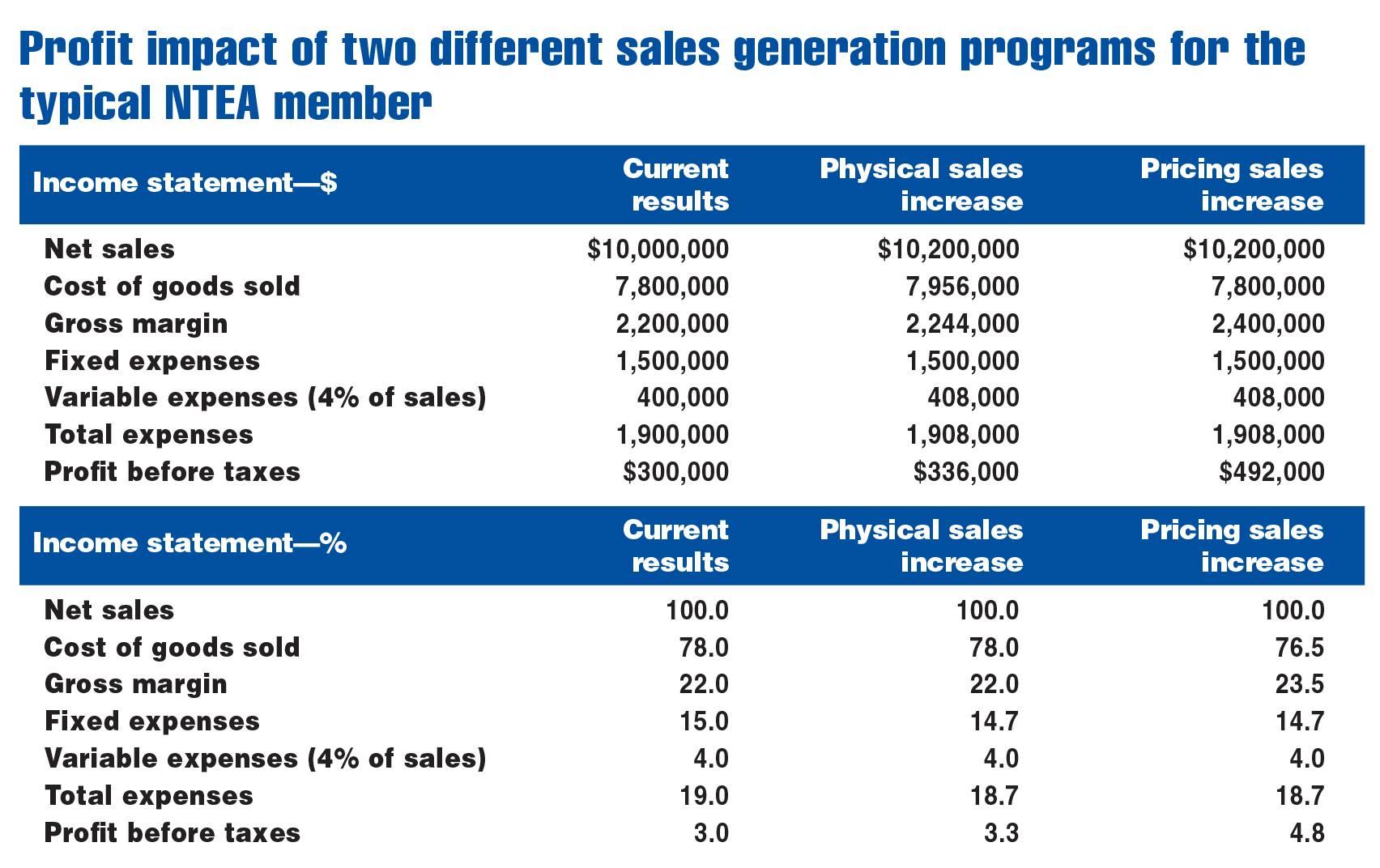

Effects of different sales strategies

The chart above reflects an income statement for the typical NTEA member company. As shown in the first column, the firm generates $10 million in sales and operates on a gross margin of 34% of sales and 19% expenses. This results in $600,000 pre-tax profit or 4% of sales.

To understand how different sales-generation strategies impact profit, expenses must be split into two categories — fixed and variable. Many businesses do not clearly recognize this distinction.

Once a budget is set for the year, fixed (or overhead) expenses will only change if management takes specific actions to do so, such as negotiating lower rent. For most companies, fixed expenses account for around 80% of total expenses — about $1.5 million per year for the typical NTEA member.

In contrast, variable expenses (sales commissions, interest on accounts receivable, etc.) rise and fall automatically with sales. They’re estimated to be 4% of sales for the average firm.

The second column of numbers examines the impact of selling 2% more merchandise. As shown, sales, cost of goods sold, gross margin and variable expenses increase by 2%, while fixed expenses remain constant. As a result, profit increases from $300,000 to $336,000, or 12%.

While 12% is impressive, it differs from the effect of a price increase that would generate the same level of sales volume (demonstrated in the chart’s last column).

As illustrated, sales increase by 2%, but cost of goods remain the same. This causes gross margin dollars to increase by 9.1% rather than the 2% gain from more physical sales activity. The difference may seem small, but has major implications for profit.

The last column reflects variable expenses rising with sales and fixed remaining constant. This means most of the gross margin increase will fall through to the bottom line — resulting in $492,000 profit before taxes (a 64% gain).

Simply put, both changes result in the same level of dollar sales. However, one produces a 12% profit increase and the other a 64% jump. How sales growth is generated can be a key determinant of profit.

Actions to help achieve profitable sales

A predictable, yet legitimate, response to the third column of numbers is that it can’t be done. In a competitive market, piling on even small price increases across the board is challenging. Something else needs to happen, which requires three different actions.

Working with the sales force

One of the biggest barriers to enhancing gross margin is the tendency of some salespeople to cave in when confronted with price objections. This is partly because many customers continually push for lower-price opportunities, eventually causing salespeople to believe prices really are too high.

At the same time, research shows customers are actually less price-sensitive than salespeople. Buyers are simply doing what they should — seeing if lower prices are available. They’re not necessarily convinced they can get a price reduction, but are merely investigating.

A potential solution is to provide continual training to help the more susceptible salespeople overcome price objections.

Strategic pricing

One strategy that has been recommended over the years is to raise prices on the slowest-selling, and probably least price-sensitive, items. An underlying issue is there are multiple SKUs in the slow-selling category (half the product line for most companies). As a result, it’s considered too much work for too little improvement. Some businesses that have made the effort, though, have reported a significant increase in overall gross margin percentage without the loss of any physical sales volume.

Linking price to service

A key challenge is linking prices charged to customers to the cost of servicing those buyers. Research shows some customers have an exceptionally high cost of service. This can occur with accounts that place multiple small orders, have numerous emergency orders or overload the returns process. The concept is easy to comprehend, but the cost is difficult to calculate.

As such, it may seem easier to avoid the entire issue. Again, though, research indicates differences in cost to service are seldom accounted for in pricing. With current technology, calculating cost to serve is becomingly progressively easier. Resulting analysis suggests services should be lowered or prices increased.

Moving forward

Pricing remains an important profitability driver for distribution companies. It’s essential to focus not just on increasing sales, but on boosting profit while doing so.

Visit ntea.com/profitreport for more articles.