By Steve Latin-Kasper

NTEA Director of Market Data & Research

This article was published in the August 2016 edition of NTEA News.

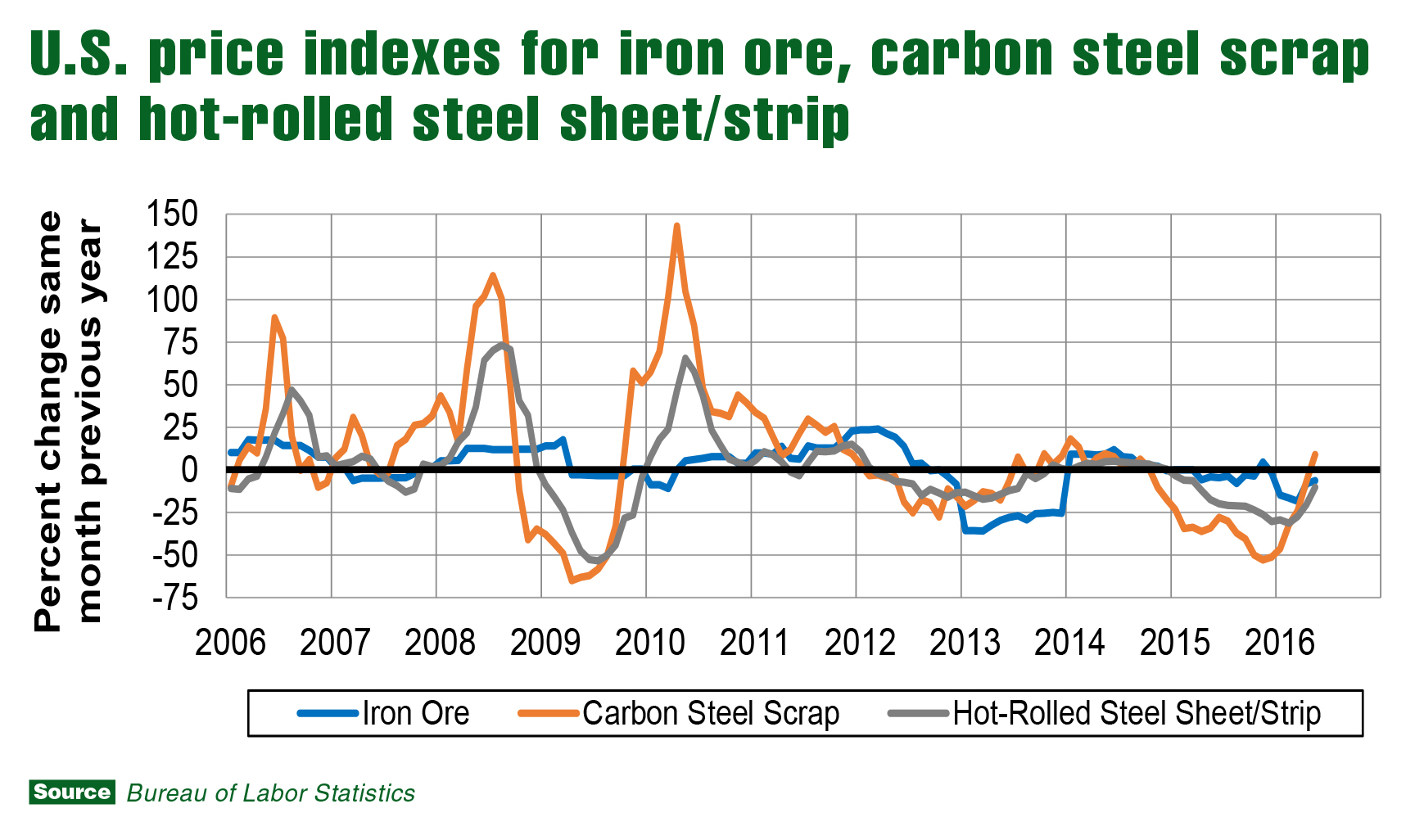

Steel prices started climbing in the first half of 2016 after trending down since the fourth quarter of 2014. Between January and May, the U.S. price of hot-rolled steel sheet/strip rose 9.3 percent on a month-to-month basis, according to the Bureau of Labor Statistics. Prices are expected to rise again in June.

This increase was expected, but not until at least the second half of 2016 when global economic growth was anticipated to improve and generate enough demand to influence overcapacity in the steel industry. However, economic activity in China, which is home to half of the global steel market’s capacity, expedited the process.

As shown in the chart below, carbon steel scrap prices rose in May 2016 compared to the same month in 2015, marking the first yearly increase since 2014. This is important since price changes in the carbon steel scrap sector tend to lead shifts in other steel market prices. Iron ore and sheet/strip prices started rising shortly after.

What put this chain of events in motion? The answer is five consecutive years of decline in the Chinese market for reinforcement bars as their real estate industry cooled off. Normally, rebar inventories would top off in the winter to prepare for the spring building season. However, low expectations for 2016 led to a muted inventory level. At the same time, the Chinese real estate market revived, pushing up costs for housing and construction materials. Spot prices for rebar rose almost 50 percent by the end of April on the Shanghai Exchange.

None of this changes the fact that there is still overcapacity in the global steel sector. However, growth in the U.S. and European Union (EU) economies increased demand for steel as well. Also, a revival in oil prices brought increased demand for steel and most other commodities in Russia and the Middle East. As a result, steel product inventories were low in other geographic markets in addition to China.

Expectations

Steel prices will likely keep climbing entering the second half of 2016. The EU and U.S. economies are expected to continue growing — albeit slowly — this year and next. The price of oil should remain fairly stable through 2017, which means oil-based economies will probably increase their demand for steel as well.

Last, but far from least, is China’s impact on the global market going forward. While reports indicate the economic growth rate trended down in China over the past year, its economy grew at a 6.7-percent rate in the first quarter — which means the only large economy experiencing faster growth is India.

Apparently, though, 6.7 percent isn’t enough. The Chinese government announced an economic stimulus plan in the second quarter. They intend to increase federal deficit to invigorate the construction market by making credit more obtainable and investing in public infrastructure. Some economists are on record saying a debt-fueled stimulus plan will ultimately backfire in the form of a recession. On the other hand, China is sitting on $2 trillion of foreign reserves, so it can afford to take on some debt.

In sum, steel prices should keep rising in the second half of 2016 as the global economy continues to grow. The good news is, the overcapacity should prevent price increases from becoming unmanageable.

If you have any questions, contact Steve Latin-Kasper at 248-479-8193 or email stevelk@ntea.com.